On April 17, millions of American taxpayers will file their income taxes. A small fraction of these individuals could be in for a nasty surprise. Last year saw millions of people jump onto the cryptocurrency train, purchasing countless cryptocurrencies. Unfortunately, most buyers probably didn’t realize their purchases are taxable, depending upon gains and losses. A note from the Internal Revenue Service in 2014 provides the only guidance on the matter, and taxpayers are expected to follow this mandate.

Taxpayers need to know what they bought a given cryptocurrency for, and what amount it was sold for as well. In fact, it doesn’t matter whether the cryptocurrency was exchanged for US Dollars or another cryptocurrency. Individual taxpayers are expected to track all of these transactions, whether it’s one transaction or a thousand transactions. The sum of these transactions are then reported as either an overall gain or loss. Someone with a net gain would have to pay the current capital gains tax rate.

Currently, the IRS treats cryptocurrencies as property. Taxpayers can purchase a currency and hold onto it without much of a tax obligation. Things change the second that currency is exchanged back into dollars, or into another currency, though. Seasoned investors would expect nothing less than this, but casual buyers might be shocked. Without a doubt, strict record keeping is necessary to avoid problems here. Even a handful of cryptocurrency transactions could land someone in hot water with the IRS.

It’s 100% legal to buy and sell cryptocurrencies (except one) in the United States. All of these transactions are akin to buying and selling stocks. If someone is audited by the IRS and hasn’t reported these transactions, then they’re going to face problems. Typically, consequences will range from tax penalties to more severe lawsuits. An audit will reveal cryptocurrency dealings, and negligence or ignorance won’t work as excuses. A Bitcoin millionaire that hasn’t reported the income could lose thousands of dollars.

In the end, most cryptocurrency exchanges provide a detailed record of one’s transactions. Taxpayers need to realize the tax situation they find themselves in for buying and selling cryptocurrencies. Even the smallest transactions need to be reported to the IRS in order to avoid problems during an audit. Otherwise, a given taxpayer could find themselves losing a lot of money, or even facing jail time in severe cases.

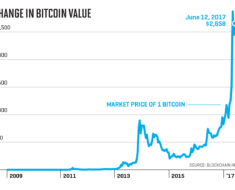

Cryptocurrencies are an excellent investment tool, but they’re treated just like any other investment option for tax purposes.

Dil Bole Oberoi